English

English

Spanish

Spanish

Portuguese

Portuguese

More Players, Less Business Value: The Acquisition Problem in the iGaming Industry

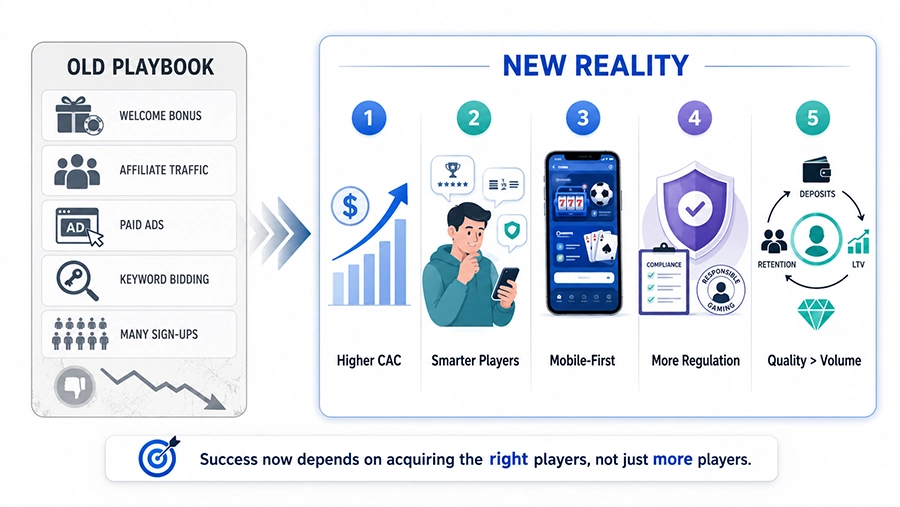

For years, player acquisition in iGaming followed a relatively predictable playbook: aggressive bonuses, broad media buying, extreme focus on first-time deposits, and much more. Scale was the metric. More traffic meant more players and hence more growth.

Today, by most conventional measures, iGaming is growing, attracting new players, entering new markets, and generating significant revenue worldwide. On paper, the industry’s growth is compelling.

Yet, the underpinning environment has changed significantly. The industry is entering a more mature phase, where profitability, retention, compliance, and player quality matter far more than just raw acquisition numbers. Rising acquisition costs, tighter regulations, changing player expectations, and increasing competition are forcing operators to rethink how they attract and retain users.

The question, as a result, has shifted from the quantity of players acquired to the quality of those acquired.

Behind the industry’s continued growth is the more sobering realisation that the cost of bringing a new player through the door is rising sharply, while the channels that once delivered efficient growth are saturating or constrained by regulatory pressure. At the same time, the players are more informed and mobile-native and thus less loyal to individual brands than before, making them difficult to acquire and even harder to retain.

Player acquisition, by its nature, has always been competitive. Acquiring high-quality players in a sustainable, compliant, and profitable manner has become significantly more challenging, and understanding why this is now a business imperative.

What Has Changed: The Industry Has Outgrown Traditional Acquisition Thinking

The iGaming industry today is fundamentally different from what it was a decade ago. Back then, the playbook was relatively straightforward. Launch a platform, structure a generous welcome bonus, seed your presence across affiliate networks, bid on high-intent keywords, and watch the first-time depositors roll in.

Many of the frameworks still used across the industry were developed for a market that looked different from today’s environment. That era is not over, but its margins have collapsed.

Today, several structural shifts are reshaping the player acquisition landscape.

The first is the increasing cost of visibility. Digital advertising ecosystems have become significantly more competitive, with more operators competing not only against other gaming brands but against virtually every consumer-facing industry bidding for the same audiences. As customer acquisition costs rise, inefficient spending becomes increasingly difficult to justify.

The second shift is the growing maturity of the players themselves. The player profile, too, has fundamentally shifted.

Gen Z now represents an increasingly important segment of the global iGaming market, bringing in a distinct set of expectations. They value instant payouts, seamless mobile journeys, social-first experiences, and personalized engagement. They have low patience for generic, transactional relationships with platforms.

More broadly, modern players are mobile-first, highly informed, and more selective in their choices. They are less likely to remain loyal to a platform solely owing to its welcome or bonus offer. Instead, they compare experiences across multiple operators and make decisions based on factors such as product quality, user experience, convenience, trust, and the overall value delivered by the platform.

Another shift is that mobile is becoming the dominant surface. The majority of players now access platforms via smartphones or tablets, and in some markets, it is closer to 60-80%. The infrastructure of acquisition, including creative assets, landing pages, and onboarding flows, must all be built mobile-first. What works on a desktop increasingly falls flat on a 6-inch screen.

Regulatory developments are reshaping the rules of engagement. Transforming compliance requirements, responsible gaming obligations, and restrictions on advertising practices in various jurisdictions have reduced the effectiveness of acquisition tactics. Operators cannot just rely on aggressive promotional strategies as primary growth drivers.

Perhaps most importantly, business priorities have evolved. Registration numbers alone are no longer considered a reliable indicator of success, and metrics carry far greater strategic importance. This evolution fundamentally changes how operators think about acquisition.

The Hidden Cost of Chasing Volume: Why Sticking to Older Methods Is Costing You Player Quality

Much of the conversation around player acquisition focuses purely on rising acquisition cost. While that challenge is important, it misses the more consequential issue: the quality of the players many of these strategies attract.

Many operators continue to rely on player acquisition tactics that were designed for a very different market. On the surface, these methods still look effective; registration volumes remain healthy, conversion rates look positive, and campaign reports suggest strong performance, but these metrics often conceal deeper inefficiencies.

When strategies prioritize volume over quality, they frequently attract players with little intention of becoming long-term customers. The industry’s long-standing reliance on aggressive welcome offers illustrates this challenge well. While these incentives can be effective at driving registrations and first-time deposits, they often attract bonus-driven users who move between platforms seeking short-term promotional value rather than meaningful engagement.

These players may register, claim bonuses, make minimal deposits, and churn shortly afterward. While this inflates the acquisition metrics, it rarely translates into profitable revenues or long-term customer value.

The hidden costs of this approach accumulate quickly.

Marketing budgets become diluted as resources are directed toward audiences with limited long-term value. Customer support, CRM, and retention teams spend time and effort engaging players who are unlikely to remain active, and over time, acquisition spending increases while the quality of the acquired cohort depletes.

Bonus abuse further compounds the problem. Incentive-heavy acquisition strategies can attract users whose primary objective is to extract promotional offers rather than participate in the gaming ecosystem. Fake sign-ups and bot traffic can inflate performance metrics while contributing little meaningful business value.

Another challenge lies in how acquisition success is measured. Many operators still rely on these short-term metrics of registrations, first-time deposits, etc. While these indicators provide visibility into conversion activity, they often reveal very little about long-term player quality. Channels that appear highly effective based on volume may ultimately deliver poor retention, low engagement, and weak lifetime value, and this creates a risky cycle as it leads players to churn quickly, which in turn forces the operators to keep reinvesting into acquisition budgets. Thus, rather than building a growing player base that generates sustainable growth, they are trapped in refilling the bucket. It eventually leads to a significant gap between acquisition cost and actual business value.

Further, regulatory pressure adds another layer of complexity. As responsible gambling frameworks evolve across global markets, broad and untargeted acquisition practices are coming under greater scrutiny, these are conflicting with evolving expectations around player protection, responsible marketing, etc.

Without visibility into long-term player quality, operators risk scaling inefficiencies rather than growth.

As competition intensifies, this approach becomes increasingly unsustainable. The operators achieving the strongest results today are not necessarily those spending the most on acquisition. They are the ones making smarter decisions about where, how, and why they acquire players, with a clear focus on long-term player value rather than short-term volume.

What Works Today: The New Acquisition Playbook

In today’s environment, the most effective acquisition strategies are built around intelligence and not reach alone. The operators gaining ground are those who have moved beyond channel-led thinking to relationship-led thinking. The distinction matters.

The industry’s acquisition mix is becoming increasingly diversified. Operators are expanding beyond traditional performance marketing channels to reach players earlier in their decision-making process.

Community-driven acquisition is gaining momentum. Mobile-first players spend significant amounts of time on social platforms and want to engage with games through platforms they already inhabit. Operators that build meaningful presence within these ecosystems are more likely to engage potential players before they reach the point of conversion. This approach creates acquisition pipelines that are often more cost-effective and more resilient than relying solely on search or paid advertising.

At the same time, content-led marketing is emerging as a valuable acquisition lever, particularly for younger, modern demographics. Unlike traditional advertising, high-quality content helps build better credibility, brand familiarity, and trust by providing genuine value to potential players. Educational resources, market insights, game guides, and other informative content can engage audiences long before they actually register.

SEO and organic content continue to offer long-term value for operators willing to invest consistently. In a market where paid media costs are inflating, building visibility around high-intent searches creates a durable acquisition asset, organically. Strong content strategies not only drive traffic but also help establish trust and authority that play a major role in player decision-making.

Localisation is also a critical competitive advantage. As operators expand into emerging markets, success often goes beyond just translating content or supporting local payment methods. New regions require a deeper understanding of local player behavior, cultural preferences, regulatory requirements, and market expectations. Operators investing in genuine localisation are better positioned to acquire and retain players over a longer term.

However, channel diversification alone is not enough. The real advantage comes from understanding which players each channel attracts and how those players behave after acquisition.

Leading operators view acquisition as a starting point of the customer relationship rather than a standalone marketing objective. Instead of optimizing for acquisition alone, they measure acquisition efforts on levers such as retention, engagement, and lifetime value. This shift has also transformed how acquisition performance is measured.

Audience segmentation and personalization have become equally important. Rather than targeting a broader audience, operators are using behavioral insights, player preferences, and engagement patterns to identify and attract players who are most likely to become loyal customers. Acquisition campaigns are increasingly tailored to specific audiences, creating more relevant experiences from the very beginning.

At the center of this is first-party data. It has become a key competitive advantage, enabling operators to better understand their audiences and drive more precise targeting, stronger personalization, improved retention, and reduced reliance on increasingly restrictive third-party acquisition channels.

The result is a significantly different acquisition strategy from the one defined in the industry’s earlier growth phase. Success increasingly belongs not to the operators who can generate the most traffic, but to the ones who can build lasting relationships and create longer lifetime value.

Conclusion

The evolution of player acquisition reflects a broader shift that is taking place, as markets are maturing and competition is intensifying, growth is becoming less about attracting attention and more about earning relevance.

Perhaps the biggest misconception in iGaming is that player acquisition remains primarily a growth challenge and not an allocation challenge. In reality, it has become an exercise in capital allocation. Every acquisition strategy reflects a series of choices about where resources are invested and which audiences are prioritised.

In contrast, microservice-based architectures are better suited to support this approach. By breaking the platform into smaller, independent services, microservices allow different components to operate, scale, and evolve separately. This makes it easier to integrate with external systems, whether for analytics, player engagement, or AI-driven capabilities. New tools can be connected without requiring extensive changes across the entire platform.

This shift changes the nature of competition. The operators who succeed over the decade will be those who develop a deeper understanding of player behavior and build systems capable of turning that understanding into long-term relationships. In an industry where acquisition channels become more expensive and regulatory environments more demanding, sustainable growth will belong to operators with the ability to allocate resources intelligently, which may prove far more valuable than the ability to acquire at scale.

Learn more about Skilrock here: www.skilrock.com